Climate Change and Insurance: A Shared Responsibility to Protect the Public

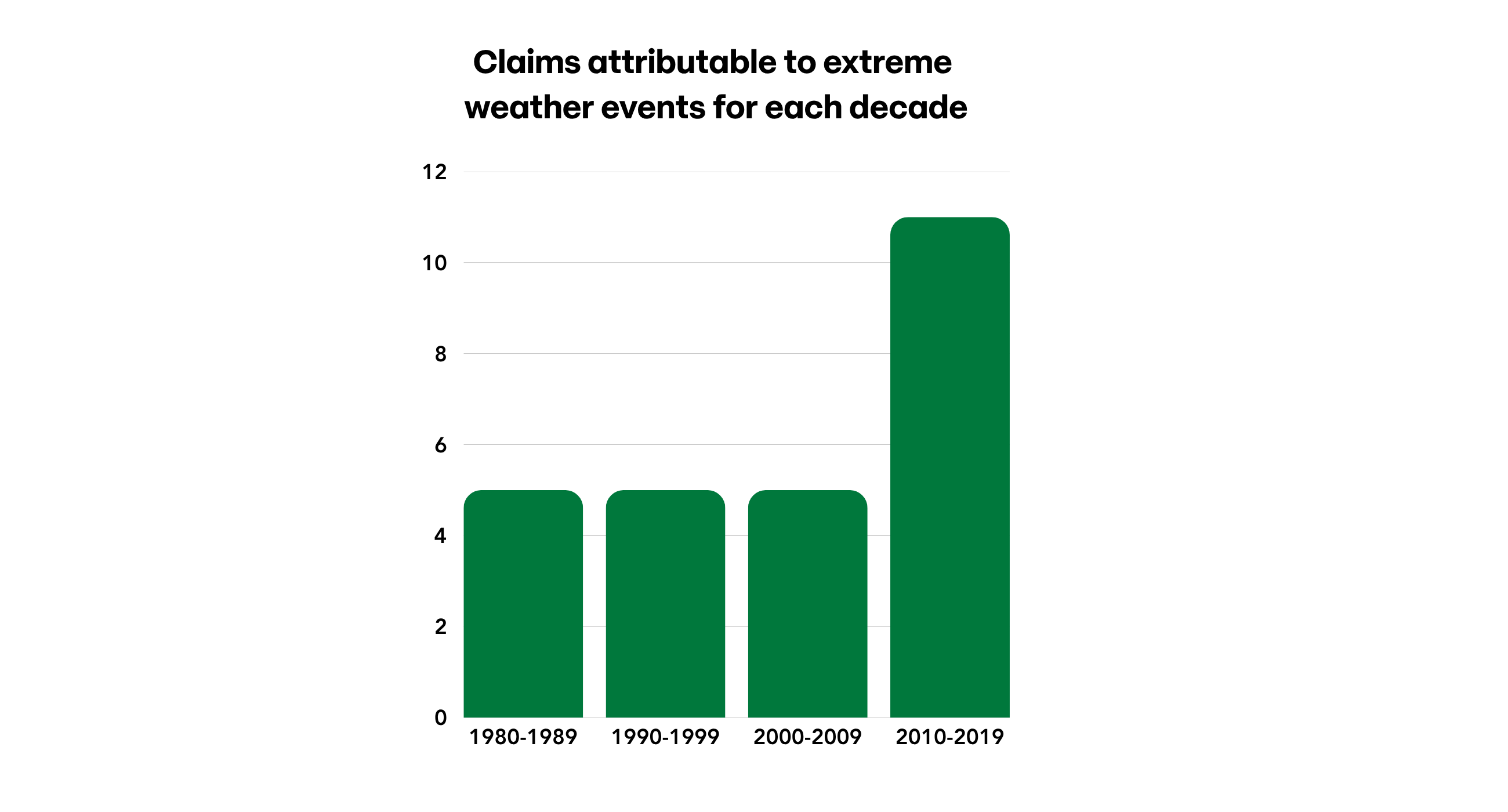

Climate change and the risks it generates are no longer hypothetical. Over the past two decades, losses caused by weather-related disasters have increased significantly (see the graph below¹). According to the Insurance Bureau of Canada2, “The summer of 2024 stands out as the most destructive season in Canadian history for insured losses,” notably due to the Calgary hailstorm and Hurricane Debby in Quebec.

Beyond the figures, these events deeply disrupt the lives of those affected, who suffer both financial and psychological consequences. Protecting consumers and their assets must therefore remain a top priority for the financial industry.

In this context, who is responsible for taking action? How can financial industry stakeholders contribute to better protecting the public?

La Chambre de l’assurance examined these questions through the lens of shared responsibility. Ms. Jannick Desforges, LLB, Director of Legal Affairs, presented these reflections at the conference Régulation financière : une alliée face aux changements climatiques ?, held by the Laboratoire en droit des services financiers (LABFI) on October 30, 2025.

This article highlights key takeaways shared by several speakers and explores the critical role played by agents and damage insurance brokers, and claims adjusters.

Understanding Contracts and Risks: A Major Challenge

First, it is important to examine a significant issue: consumer confusion around risks and insurance.

“Who truly understands their insurance contract?” Ms. Desforges asked (our translation). This is far from a trivial question, given that 50% of insured individuals who read their policy do not understand it³.

In a climate change context, if an insurance contract is unclear, how can consumers, when faced with extreme weather events, know what coverage they have and understand its limits and exclusions? Many grey areas remain, such as:

- How can one know whether their home is located in a flood zone?

- Why does an insurer refuse to offer certain coverage to some clients?

- How can the proper amount of insurance needed to rebuild a home or replace belongings after a loss be calculated?

- Is sewer backup risk limited to ground‑level dwellings?

“There is a significant information imbalance between the insurer, who drafts the contract, and the consumer, who purchases the service. The role of the professional is precisely to reduce that imbalance by informing, explaining, and advising the consumer,” Ms. Desforges emphasized (our translation).

Real Case: A Depreciation Clause in an Insurance Contract

A revealing example comes from the television program La facture, aired on March 18, 2025⁴. A policyholder was affected by the 2024 Calgary hailstorm, which completely destroyed her roof. The total repair cost amounted to $50,000, yet the insurer paid only $12,000. Why? A depreciation clause in the insurance contract stated that the 10‑year‑old roof had lost 50% of its value. Unsurprisingly, the policyholder was unaware of this clause.

Three key observations emerge from this situation:

1. The agent or broker did not inform the insured at the time the policy was purchased.

2. The insured did not read or fully understand every clause of the contract.

3. This type of clause is generally unknown to the average consumer.

Special Attention to Water Damage

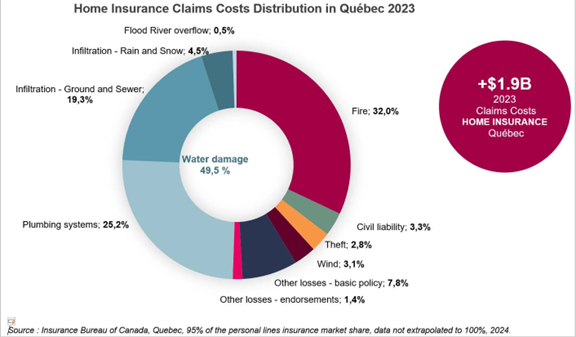

When discussing risks and coverage, special attention should be paid to water damage. According to the Insurance Bureau of Canada, 50% of home insurance claims relate to water damage⁵. Half of these claims are associated with weather events, including water infiltration and river flooding.

When discussing risks and coverage, special attention should be paid to water damage. According to the Insurance Bureau of Canada, 50% of home insurance claims relate to water damage⁵. Half of these claims are associated with weather events, including water infiltration and river flooding.

These data clearly demonstrate the importance of educating and equipping consumers regarding water‑related risks.

Shared Responsibility: A Role for Everyone

A consensus emerged during the LABFI conference: protecting consumers in a changing climate is everyone’s responsibility. Governments, regulators, the financial industry, and consumers all have a role to play.

Mathieu Boudreault, Professor of Actuarial Science at UQAM, summarized the division of responsibilities as follows:

- Municipalities: land‑use planning and infrastructure maintenance

- Provincial government: oversight of municipalities, flood‑zone mapping, and (limited) financial assistance of last resort.

- Federal government: financial support to provinces and municipalities through various programs, including:

- Disaster Financial Assistance Arrangements (DFAA).

- Funding programs aimed at climate adaptation.

- Financial services industry: insurers, who offer insurance products, and banks, which provide mortgage products.

For her part, Jannick Desforges grouped responsibilities into three categories: design, information, and prevention.

Design

Product design primarily concerns insurers. According to Ms. Desforges, insurers should:

- Take client needs and interests into account when developing products.

- Simplify insurance contracts, coverage wording, and endorsements to improve comprehension.

- Offer coverage that encourages rebuilding in a more resilient manner.

France LeBlanc, Strategic Advisor at Beneva, noted that “insurers are already taking action in areas they can control” (our translation). She identified six key levers available to insurers:

1. More sophisticated risk assessment, enabling refined mapping and pricing that better reflects exposure levels.

2. Differentiated deductibles for water damage, fostering shared responsibility and encouraging preventive measures.

3. Premium discounts for clients who install prevention devices.

4. Real‑time weather alerts, offering guidance on immediate actions to reduce potential damage.

5. Resilient coverage, which goes beyond simple replacement and promotes stronger, more durable rebuilding. “There is still room for evolution in insurance contracts,” she noted (our translation).

6. Circular economy approaches, encouraging policyholders to repair damaged property rather than replace it following a loss.

Information

Providing information to consumers falls largely — though not exclusively — within the role of damage insurance agents and brokers. This information enables insureds to make informed decisions. According to Ms. Desforges, this involves:

- Strengthening the advisory role of certified professionals to help them better inform, explain, and advise insureds regarding natural disasters.

- Paying close attention to changes in contracts and evolving client needs.

- Guiding consumers toward effective preventive measures.

Prevention

Prevention and resilience are shared responsibilities among consumers, insurers, and governments.

Consumers

- Learn about risks, choose appropriate coverage, and implement preventive measures to reduce loss impacts.

Governments

- Offer financial incentives for resilient home renovations, similar to existing « Réno‑vert »–type programs.

- Invest in the adaptation of public infrastructure (e.g., sponge streets and alleys).

- Prohibit rebuilding in flood‑prone or very high‑risk areas.

- Update building codes.

Insurers

- At underwriting: provide incentives for policyholders who have already implemented resilience and prevention measures.

- At claim time: allow rebuilding or renovation using resilient materials.

In this context, Gabriel Lévesque‑Lessard, Financial Institutions Compliance Analyst (our translation) at the Autorité des marchés financiers, presented the Guideline on the Management of Climate Change Risks. This document outlines the regulator’s expectations for the industry, including insurers. It defines the principles guiding the identification, assessment, and management of climate‑related risks while allowing organizations sufficient flexibility to tailor their approach to their business model. The guideline highlights internationally recognized practices, particularly with respect to governance, climate scenarios, and transparency.

From the perspective of conference speaker Loïc Geelhand de Merxem, Ph.D. in Securities Law and Corporate Governance Analyst in the French market, a shift is needed from an obligation to “disclose” to an obligation to “act.” Given the unpredictability of future climate impacts, he argued that regulators should take a firmer stance, noting that current approaches remain relatively gentle.

Best Practices for the Advisory Role

“Insurance requires specific expertise. Agents and brokers must pass examinations with the Autorité des marchés financiers and are subject to ethical obligations and continuing education requirements. They possess knowledge that consumers do not,” Ms. Desforges emphasized (our translation) The role of a certified professional is therefore to inform and advise — not simply to find the lowest price.d’assurance, ou le lisent en partie et que 72 % préfèrent obtenir des conseils de la part d’un professionnel6, l’importance du rôle-conseil du professionnel en assurance ne fait plus aucun doute.

With 80% of Quebecers either not reading their insurance policy or reading it only partially, and 72% preferring to receive advice from a professional⁶, the importance of the advisory role in insurance is undeniable.

La Chambre de l’assurance has identified several key practices for agents and brokers to effectively support clients in managing climate‑related risks:

1. Assess the consumer’s situation by asking the right questions. Therefore understanding their needs and advising them adequately.

2. Communicate information using clear, plain language.

3. Ensure the consumer understands the product being purchased, including its limits and exclusions.

4. Explain the potential consequences if advice is not followed, such as refusing to purchase an endorsement.

5. Provide examples of preventive measures that can reduce damage.

In short, the better-informed consumers are, the better equipped they are to make sound decisions to protect their assets.

Remember: the worst situation for a consumer is believing they are adequately insured against a risk when they are only partially insured — or not insured at all.

Remember: the worst situation for a consumer is believing they are adequately insured against a risk when they are only partially insured — or not insured at all.

Ressources

Tip: Use existing tools to help you in your advisory role. Here are some examples:

Tip sheet to share with clients: Climate change: insurance coverage and preventive measures, outlines the main climate-related risks covered under a basic insurance policy and those that can be added through a supplementary endorsement, along with questions to consider and preventive measures to help mitigate the risk of damage and financial loss.

Climate change training: These training activities provide practical tools to help certified professionals better support their clients in addressing climate and natural hazards (in French only).

- Sinistres liés aux tremblements de terre

- Sinistres liés au feu

- Sinistres causés par le vent

- Sinistres causés par l’eau

Natural Disasters section of the Insurance Bureau of Canada website.

Conclusion: Let Us Act Together

As Mathieu Boudreault pointed out, “in Quebec and elsewhere, we are seeing insurers withdraw from certain neighbourhoods” (our translation). This sends a strong signal of the urgency for governments and other sectors to act.

He also raised the growing challenge of insurability — the increasing difficulty for citizens to obtain adequate insurance at a reasonable price or to receive government assistance when needed.

If no action is taken, we may reach the breaking point⁷ mentioned by France LeBlanc, where insurance becomes inaccessible or unaffordable for many citizens.

According to Ms. Desforges, in such a scenario, consumers would be the greatest losers. As risks and losses intensify, insurers may be forced to:

- Increase premiums.

- Reduce coverage limits.

- Refuse to offer certain types of coverage.

- Decline policy renewals.

- Withdraw from specific markets.

To protect the public, everyone must therefore act according to their role, responsibilities, and area of expertise.

The translation of this article was done using AI but was reviewed by humans.

[1] ICanadian Climate Institute. (2020). Final Report of the Canadian Council on Climate Change [PDF]. https://institutclimatique.ca/wp-content/uploads/2020/12/COCC-Final-FRENCH-1209.pdf

[2]Insurance Bureau of Canada. (2025). Review of Natural Disasters: Press Release of January 13, 2025 [PDF]. ibc_nr-2025-01-13_natcat_wraprelease_fr.pdf.

[3] Chambre de l’assurance de dommages. (2014). Une personne sur quatre n’a pas l’esprit tranquille une fois assurée. Et vous? [PDF] (in French). depliant-consommateur-2014.pdf.

[4] Radio-Canada. (2025). La facture – Assurance habitation, changements climatiques et consigne [Episode March 18, 2025]. https://ici.radio-canada.ca/tele/la-facture/site/episodes/1012063/assurance-habitation-changements-climatiques-consigne-expiration

[5] Insurance Bureau of Canada. (2023). Home Insurance Claims Costs Distribution in Quebec 2023 [PDF]. https://infoassurance.ca/media/rxkddcwn/cout-sinistres-habitation-quebec_2023_en.pdf

[6] Chambre de l’assurance de dommages (ChAD). (2018). Assurances : le conseil professionnel essentiel, disent les Québécois [Article Web]. (In French) https://chad.ca/actualites/2018/05/assurances-le-conseil-professionnel-essentiel-disent-les-quebecois

[7] Eberle, C., O’Connor, J., Narvaez, L., Mena Benavides, M., & Sebesvari, Z. (2023). Interconnected Disaster Risks 2023: Risk Tipping Points. United Nations University – Institute for Environment and Human Security (UNU‑EHS).

Related articles

Protection of personal information: reminders and new concepts

What to Do When the Quotes Differ

Financial and material maltreatment* : what should you do?

Cybersecurity: best practices to follow

Your Questions: Which Acts Are Reserved for Agents and Brokers?

Which Acts Are Reserved for Agents and Brokers?

An Overview of Deductibles for Syndicates of Co-ownership

Private or Public Insurance: Effectively Assisting Your Client After a Flood